The Truth About Mortgage Rates: Why MBS Markets Matter More Than the Fed

Every time the Federal Reserve announces a rate cut, you'll see headlines screaming "Fed Cuts Rates! Check Your Mortgage Rate Today!" Here's the truth that most people—and unfortunately, many in my industry—don't understand: the Fed Funds Rate does NOT directly control mortgage rates. What does? Mortgage Backed Securities (MBS).

I've been in this business for over 20 years, and one of the most common misconceptions I encounter is that the Federal Reserve controls mortgage rates. Let me share how understanding MBS markets helped one of my clients save over $200 per month on their refinance.

⚠️ Misleading Advertising Alert

If you see an ad saying "The Fed lowered rates—refinance now!" that's a red flag. The advertiser either doesn't understand how mortgage pricing works, or they're hoping you don't. The only mortgage products directly tied to the Fed Funds Rate are those pegged to the Prime Rate (like some HELOCs and adjustable-rate products). Traditional fixed-rate mortgages? They follow the MBS market.

A Real Client Story: Timing the MBS Market

Mike & Sarah's Refinance Win

Closed December 2025

Mike and Sarah came to me last fall looking to refinance their home in Tacoma. They had a 7.25% rate from when they bought in 2023, and with rates starting to improve, they wanted to see what was possible.

When they first called, the FNMA 5.5% coupon was trading around 99.50. I told them, "Let's get your paperwork ready, but I want to watch the bond market before we lock. I'm seeing some momentum that could work in your favor."

Over the next three weeks, we watched the MBS market together. Every few days I'd send them a quick text: "Bonds up 12 basis points today—looking good" or "Flat day, still holding." They thought it was pretty cool to see behind the curtain.

Then one Tuesday morning, I saw the jobs report came in weaker than expected. MBS prices jumped. I called Mike immediately: "Lock now. Bonds are up 38 basis points from where we started. This is our window."

We locked at 5.875%—down from the 6.375% that was available when they first called. On their $425,000 loan, that's $218 less per month and over $78,000 in lifetime savings.

"Emmett actually explained what was happening in the bond market and why we should wait. When he said it was time to lock, we trusted him completely. Best decision we made—we're saving over $200 a month compared to if we'd locked on day one."

— Mike T., Tacoma, WA

What Are Mortgage Backed Securities?

When you get a mortgage, your loan doesn't just sit on a bank's books forever. Most mortgages are packaged together and sold as bonds to investors on Wall Street. These bonds are called Mortgage Backed Securities (MBS), and they're primarily issued by government-sponsored enterprises like Fannie Mae and Freddie Mac.

Every day, traders buy and sell these MBS bonds just like stocks. The prices fluctuate based on economic news, inflation data, employment reports, geopolitical events, and investor sentiment. These daily MBS price movements are what determine your mortgage rate—not the Fed, not exclusively the 10-Year Treasury (though there's some correlation), but the actual bonds backed by mortgages.

Understanding MBS Coupons: The FNMA 30-Year 5.0%

MBS bonds are identified by their "coupon"—the interest rate paid to investors. Right now, mortgage professionals like myself watch coupons like the FNMA (Fannie Mae) 30-Year 5.0% because it corresponds roughly to current market rates. Understanding how to read this data is part of what I explain on my mortgage terminology page.

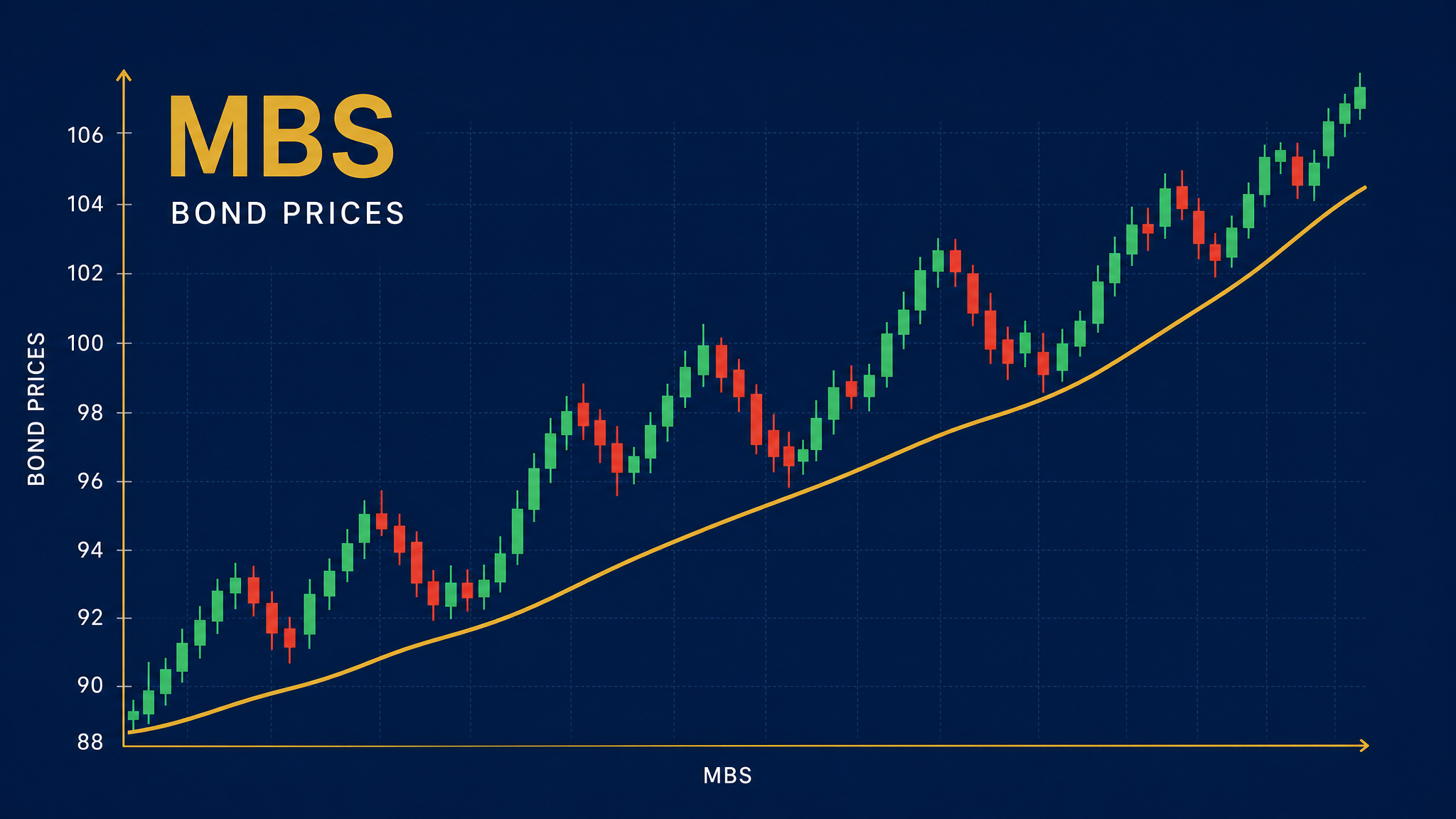

Illustrative: how mortgage-backed securities (bond) prices move

Japanese candlestick chart showing daily MBS price movements. Green candles = price increases (better for rates). Red candles = price decreases (worse for rates).

The illustration above shows how a coupon's price moves over time. Each candlestick represents one trading day. When you see green candles (prices rising), that's generally good news for mortgage rates. Red candles (prices falling) typically mean worse rates ahead.

The Golden Rule: Bond Prices UP = Better Mortgage Rates

Here's the most important concept to understand:

📈 When MBS Prices Go UP

- • Bond yields go DOWN

- • Lenders can offer LOWER rates

- • Rate sheets IMPROVE

- • Better pricing for borrowers

📉 When MBS Prices Go DOWN

- • Bond yields go UP

- • Lenders must offer HIGHER rates

- • Rate sheets WORSEN

- • More expensive for borrowers

Bond prices and yields have an inverse relationship. When investors are buying bonds aggressively (high demand), prices rise and yields fall. When investors are selling bonds (low demand), prices fall and yields rise. Mortgage rates follow yields—so we always want to see bond prices climbing. This is exactly what happened with Mike and Sarah's refinance.

Why the 10-Year Treasury Isn't the Whole Story

You'll often hear financial news reference the 10-Year Treasury yield when discussing mortgage rates. While there's correlation between Treasuries and MBS, they're not the same thing. I've seen plenty of days where:

Real-World Example

The 10-Year Treasury yield was dropping (which should mean better rates), but lender rate sheets actually got WORSE. Why? Because MBS were selling off independently. Investors were moving money out of mortgage bonds specifically, even while buying Treasuries. The MBS market has its own dynamics.

This "spread" between Treasuries and MBS can widen or tighten based on factors like prepayment risk, housing market conditions, and overall mortgage market liquidity. That's why professionals watch MBS directly, not just Treasuries. If you're curious about these dynamics, the Federal Reserve's balance sheet data shows their MBS holdings over time.

The Fed Funds Rate: What It Actually Controls

The Federal Reserve's benchmark rate—the Fed Funds Rate—is the interest rate at which banks lend to each other overnight. It directly influences:

- Prime Rate (typically Fed Funds + 3%)

- Credit card interest rates

- Some adjustable-rate mortgages (ARMs) tied to Prime

- Home Equity Lines of Credit (HELOCs) tied to Prime

- Short-term business loans

Notice what's NOT on that list? 30-year fixed-rate mortgages. Your standard home purchase loan or refinance is priced off MBS markets, not the Fed Funds Rate. This is true whether you're buying in California, Texas, or any of the 18 states where I'm licensed.

COVID-19 Era: A Case Study in MBS

Remember the historically low mortgage rates of 2020-2021? Rates briefly touched the high 2% range for 30-year fixed mortgages. During that time, mortgage professionals were watching ultra-low MBS coupons:

| MBS Coupon | Era | Approximate Rate Range |

|---|---|---|

| FNMA 2.0% | COVID Low (2020-2021) | 2.50% - 2.875% |

| FNMA 2.5% | COVID Era | 2.875% - 3.25% |

| FNMA 3.0% | Post-COVID Transition | 3.25% - 3.75% |

| FNMA 5.0% | Current (2025-2026) | 5.50% - 6.50% |

| FNMA 6.0% | Recent Highs | 6.50% - 7.25% |

Those FNMA 2.0% and 2.5% coupons were trading at premium prices because investors were willing to pay more for the safety of mortgage bonds during economic uncertainty. The Federal Reserve also launched massive MBS purchasing programs (quantitative easing), which pushed prices up and yields down dramatically.

How Rate Sheets Are Built

Every morning, lenders look at where MBS are trading and build their rate sheets accordingly. Here's a simplified view of the process—and this is exactly what I'm doing when I tell a client like Mike to "float" or "lock":

- MBS Market Opens - Traders begin buying/selling mortgage bonds around 8:30am ET

- Lenders Monitor Prices - Pricing desks watch real-time MBS movements

- Calculate Margins - Lenders add their profit margin and operating costs

- Risk Adjustments - Apply pricing adjustments for credit score, LTV, property type

- Rate Sheet Published - Loan officers like me receive pricing to quote borrowers

If MBS prices drop significantly during the day (a "sell-off"), lenders may issue a mid-day reprice—pulling the morning rate sheet and issuing worse pricing. Conversely, a strong MBS rally might trigger a positive reprice with better rates. This is why I always tell my clients: the rate you see at 9am might not be the rate at 2pm.

What Moves MBS Markets?

Understanding what drives MBS can help you time your rate lock better. Here's what I watch every day:

Factors That Help MBS (Lower Rates)

- • Weak economic data (jobs, GDP)

- • Low inflation readings (CPI data)

- • Stock market sell-offs (flight to safety)

- • Geopolitical uncertainty

- • Fed MBS purchasing programs

- • Dovish Fed commentary

Factors That Hurt MBS (Higher Rates)

- • Strong economic data

- • High inflation readings (CPI, PCE)

- • Stock market rallies (risk-on sentiment)

- • Fed rate hike expectations

- • Fed reducing MBS holdings

- • Hawkish Fed statements

Practical Tips for Borrowers

Now that you understand how rates actually work, here's how to use this knowledge when you're ready to buy a home or refinance:

Smart Borrower Strategies

- ✓ Don't wait for Fed announcements - Mortgage markets often price in Fed moves weeks in advance

- ✓ Watch for volatility - Big economic reports (jobs, inflation) can move rates significantly in hours

- ✓ Lock on green days - If your loan officer says "MBS are up today," that's often a good time to lock

- ✓ Work with informed professionals - Choose a loan officer who understands MBS markets, not just rates

- ✓ Use our calculators - Try our mortgage calculators to see how rate changes affect your payment

Frequently Asked Questions

If the Fed cuts rates, will my mortgage rate drop?

Not necessarily. Fed rate cuts affect short-term rates and Prime Rate products. Fixed mortgage rates follow MBS markets. Sometimes MBS improve after Fed cuts, sometimes they don't—it depends on why the Fed is cutting and market expectations. Check our FAQ page for more common questions.

Why do mortgage rates sometimes go UP when the Fed cuts?

This happens when MBS markets sell off despite Fed action. It could be due to inflation concerns, economic growth expectations, or the market having already "priced in" the cut beforehand.

What's the difference between MBS yield and coupon?

The coupon is the stated interest rate on the bond (e.g., 5.0%). The yield is the actual return based on current market price. If you pay more than face value for a bond, your yield is lower than the coupon. Visit our mortgage terminology page for more definitions.

How can I track MBS prices?

Professional traders use Bloomberg terminals, but sites like Mortgage News Daily show MBS trends for consumers. Your best resource? A loan officer who monitors these markets daily and can advise on timing.

Should I try to "time" my rate lock?

Within reason. Trying to catch the absolute bottom is risky—markets can turn quickly. If you're getting a rate you can afford and it meets your goals, locking removes uncertainty. That said, working with someone who watches MBS daily (like my team does) can help you make informed decisions about when to float vs. lock.

The Bottom Line

Mortgage rates are determined by Mortgage Backed Securities markets, not the Federal Reserve's benchmark rate. While the Fed's actions can influence investor behavior (and thus MBS prices), there's no direct connection between Fed Funds and your 30-year fixed rate.

The next time you see an ad claiming "The Fed cut rates—refinance today!", you'll know that's an oversimplification at best, and misleading at worst. What really matters is where FNMA and FHLMC bonds are trading.

Understanding this gives you a significant advantage as a borrower. You can make informed decisions about when to lock, understand why rates move the way they do, and work with professionals who truly understand the market—just like Mike and Sarah did.

Ready to Get Expert Guidance?

As a mortgage professional with over 20 years of experience, I monitor MBS markets daily to help my clients lock at optimal times. Whether you're purchasing or refinancing, I'll help you navigate market conditions with real expertise—not marketing gimmicks.

Emmett Clark

Licensed Mortgage Loan Officer · NMLS #233747 · 20+ Years Experience

This article has been reviewed for accuracy by Emmett Clark, a licensed mortgage professional serving homebuyers across 18 states including California, Texas, Florida, Arizona, and Colorado. Last updated: 2026-01-26.

About Emmett NMLS #233747

Emmett Clark (NMLS #233747) is a licensed mortgage professional with 20+ years of experience helping families achieve their homeownership dreams. Licensed in 18 states nationwide, Emmett specializes in finding the right mortgage solution for each client's unique situation. Powered by Loan Factory, Emmett provides access to competitive rates and a wide variety of loan programs including conventional, FHA, VA, and down payment assistance programs.

Work with Emmett