From "We Really Like This House" to Getting It Under Contract: What I Tell Every First-Time Buyer

You found it. After weeks (or months) of open houses, online scrolling, and "maybe this one?" conversations, you and your agent walk into a property and something clicks.

"We really like this house."

That sentence is where my phone usually rings. And what I tell every first-time buyer next is this:

Liking the house is step one. Getting it under contract — on terms that protect you — is a whole different skill set.

This guide walks you through exactly how the offer-to-contract process works in Southern California, what to expect at each stage, and how to avoid the mistakes that cost first-time buyers thousands of dollars (or the house itself).

Step 1: Get Your Pre-Approval Locked In (Before You Even Tour)

Before you write an offer, you need a fully underwritten pre-approval — not a pre-qualification, not a rate quote, not a "yeah, you should be fine."

A strong pre-approval tells the seller:

- You've been vetted by a lender

- Your income, assets, and credit have been reviewed

- You can actually close

In competitive Southern California markets, a weak pre-approval (or none at all) will get your offer thrown out before it's read.

If you haven't done this yet, start your pre-approval here — it takes about 15 minutes and puts you in a dramatically stronger position.

Step 2: Understand What the House Is Actually Worth

Your agent will pull comps (comparable recent sales), but here's what I tell buyers to focus on:

The Three Numbers That Matter

- List price — what the seller is asking

- Comp value — what similar homes have actually sold for in the last 60–90 days

- Your number — what the home is worth to you, factoring in your monthly payment, down payment, and how long you plan to stay

Most first-time buyers fixate on #1. Smart buyers focus on #2 and #3.

Pro tip: Use our mortgage calculator to see exactly what different offer prices translate to in monthly payments. A $15,000 difference in price might only be $80/month — or it might be a dealbreaker. Know before you offer.

Step 3: Decide Your Offer Strategy

This is where it gets real. Your offer isn't just a number — it's a package. Here's what goes into it:

The Anatomy of a Strong Offer

- Purchase price — your starting number

- Earnest money deposit (EMD) — typically 1–3% of the purchase price, shows you're serious

- Down payment percentage — affects your loan type and the seller's confidence in your financing

- Contingencies — inspection, appraisal, loan approval (these are your safety nets)

- Closing timeline — standard is 30 days, but flexibility here can win deals

- Seller concessions — asking the seller to cover some of your closing costs

What I Tell First-Time Buyers About Strategy

In a buyer's market (more homes than buyers):

- Offer at or slightly below comp value

- Keep all your contingencies

- Ask for seller concessions (closing cost credits)

- Take your time with the closing timeline

In a seller's market (more buyers than homes):

- Offer at or above comp value

- Consider a larger EMD to show commitment

- Shorten your contingency periods (but never waive them entirely)

- Be flexible on closing date

- Write a clean, simple offer — fewer asks = more attractive

In a balanced market:

- Offer at comp value

- Keep standard contingencies

- Be strategic about one or two things that matter most to the seller

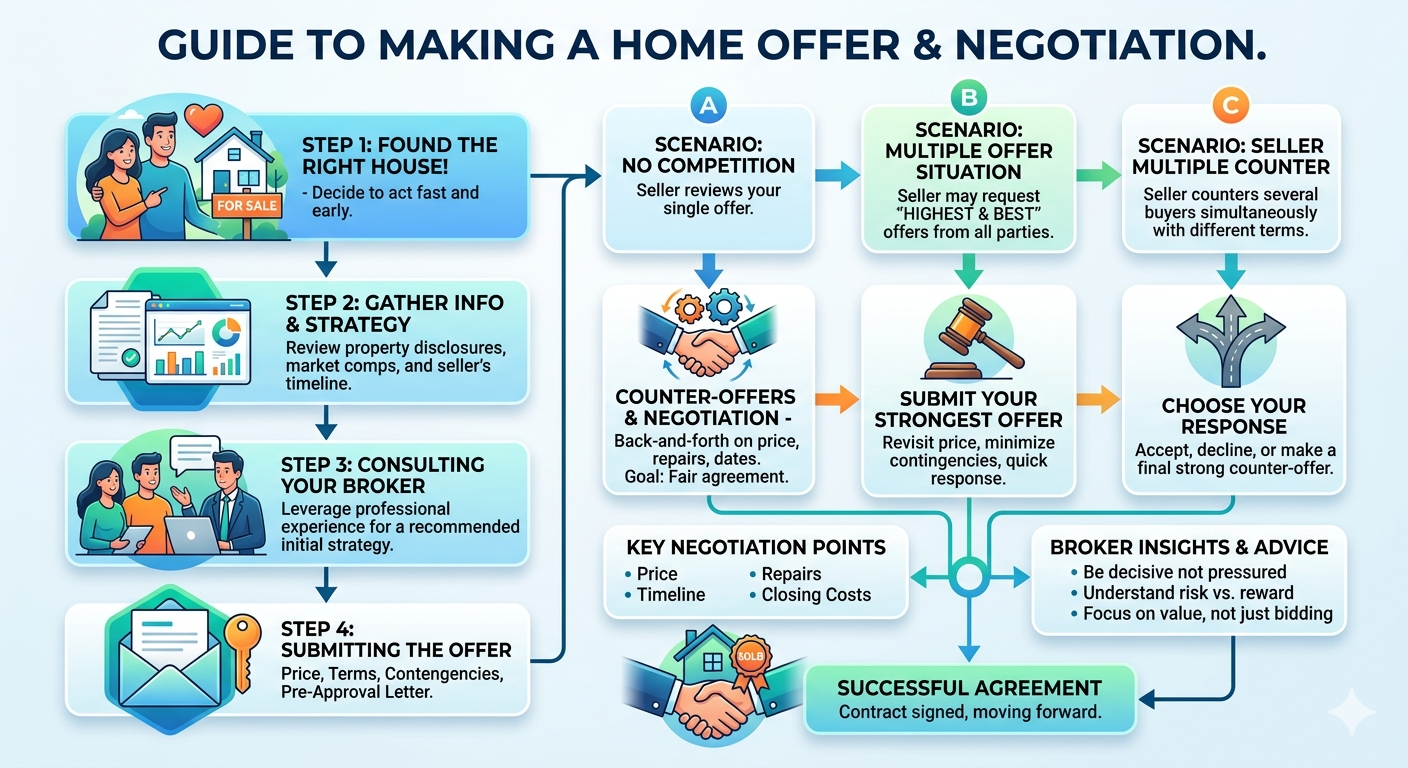

Step 4: Submit the Offer

Your agent writes up the offer using the standard California Residential Purchase Agreement (RPA). Here's what happens:

- You sign the offer — electronically, usually through DocuSign

- Your agent submits it — along with your pre-approval letter and proof of funds for your down payment

- The waiting begins — sellers typically respond within 24–72 hours

What Can Happen Next

- Acceptance — Congratulations, you're under contract! (Skip to Step 6)

- Counter-offer — The seller comes back with different terms (go to Step 5)

- Rejection — They said no. It stings, but it happens. (Go back to touring)

- Multiple counter-offer — They're countering multiple buyers simultaneously (go to Step 5, but with urgency)

Step 5: The Negotiation

This is where most first-time buyers get nervous. Here's the truth: negotiation is normal, expected, and not personal.

Common Negotiation Points

- Price — The seller counters higher, you counter back, you meet somewhere

- Closing costs — You asked for $10K in credits, they offer $5K

- Contingency timelines — They want shorter inspection periods

- Closing date — They need more time to move out

- Repairs or credits — Based on inspection findings

- Personal property — Appliances, fixtures, or furniture included in the sale

My Negotiation Rules for First-Time Buyers

- Know your walk-away number before you start. Write it down. Don't go past it in the heat of the moment.

- Respond quickly. In a competitive market, speed signals seriousness.

- Don't nickel-and-dime. Fighting over $500 when you're buying a $600,000 house can kill a deal.

- Let your agent do the talking. That's literally what they're for.

- Focus on the monthly payment, not just the price. I can often structure your loan to offset a slightly higher purchase price through rate strategies or closing cost credits.

Step 6: You're Under Contract — Now What?

Once both sides sign, you're officially "under contract" (also called "in escrow" in California). Here's your timeline:

The Typical 30-Day Escrow Timeline

Days 1–3: Open Escrow

- Escrow company is selected and opened

- You deposit your earnest money

- Title search begins

Days 1–17: Contingency Period

- Home inspection (schedule ASAP — days 7–10 is ideal)

- Appraisal ordered by your lender (I handle this)

- Review all disclosures from the seller

- Any repair negotiations happen during this window

Days 17–21: Contingencies Removed

- You formally remove your contingencies (inspection, appraisal, loan)

- This signals you're committed to closing

- Your EMD is now at risk if you back out without cause

Days 21–28: Final Loan Approval

- I push your loan through final underwriting

- You'll get a "Clear to Close" — the best three words in real estate

- Final loan documents are sent to escrow

Days 28–30: Closing

- You sign your loan documents at the escrow office (or mobile notary)

- Wire your down payment and closing costs

- The loan funds, deed records, and you get the keys

The Mistakes I See First-Time Buyers Make

After helping hundreds of first-time buyers in Southern California, here are the most common mistakes:

1. Not Getting Pre-Approved First

You fall in love with a house, rush to write an offer, and then find out you can't qualify for the amount — or your pre-approval letter takes three days to arrive while another buyer swoops in.

Fix: Get pre-approved before you tour. Period.

2. Waiving Contingencies They Don't Understand

In a hot market, some agents pressure buyers to waive inspection or appraisal contingencies. This is incredibly risky for a first-time buyer.

Fix: Talk to me before waiving anything. There are creative ways to make your offer competitive without giving up your safety nets.

3. Making Big Financial Changes During Escrow

Opening new credit cards, financing furniture, changing jobs, or making large cash deposits during escrow can torpedo your loan approval.

Fix: Don't change anything financial between offer and closing. Seriously. Not even a $200 store credit card.

4. Letting Emotions Drive the Number

"But we already told our parents about this house!" is not a reason to offer $30,000 over your budget.

Fix: Trust the numbers. There will be other houses. There won't be other bank accounts if you overextend.

5. Not Understanding Their Loan Options

Many first-time buyers don't realize they have options beyond conventional 20% down. FHA loans, VA loans, down payment assistance programs, and creative financing structures exist specifically for first-time buyers.

Fix: Talk to me about your specific situation. I'll show you every option available.

What My Role Looks Like During This Process

As your loan officer, here's specifically what I do from offer to closing:

- Pre-approval: Issue a strong, detailed pre-approval letter customized for each offer

- Offer strategy: Advise on how your financing affects your offer strength

- Rate lock: Lock your interest rate at the right time to protect your payment

- Appraisal coordination: Order and manage the appraisal process

- Underwriting: Shepherd your file through underwriting, handling any conditions that come up

- Communication: Keep you updated at every stage — you'll never wonder what's happening

- Closing: Coordinate with escrow to ensure a smooth, on-time close

- Problem-solving: When (not if) something unexpected comes up, I handle it

The Bottom Line

Getting from "we really like this house" to "we own this house" is a process — but it doesn't have to be a stressful one.

The buyers who have the smoothest experience are the ones who:

- Get pre-approved early — start here

- Understand the process — you just read this guide, so check

- Work with a lender who communicates — that's me

- Make decisions based on numbers, not emotions — use our calculators

If you're a first-time buyer in Southern California and you're getting close to writing your first offer, I'd love to walk you through it. No pressure, no sales pitch — just a conversation about your options.

Get in touch here or get a personalized rate quote to see where you stand today.

Emmett Clark is a mortgage loan officer based in Southern California, specializing in helping first-time homebuyers navigate the purchase process. NMLS #2371924.

Emmett Clark

Licensed Mortgage Loan Officer · NMLS #233747 · 20+ Years Experience

This article has been reviewed for accuracy by Emmett Clark, a licensed mortgage professional serving homebuyers across 18 states including California, Texas, Florida, Arizona, and Colorado. Last updated: 2026-04-14.

About Emmett NMLS #233747

Emmett Clark (NMLS #233747) is a licensed mortgage professional with 20+ years of experience helping families achieve their homeownership dreams. Licensed in 18 states nationwide, Emmett specializes in finding the right mortgage solution for each client's unique situation. Powered by Loan Factory, Emmett provides access to competitive rates and a wide variety of loan programs including conventional, FHA, VA, and down payment assistance programs.

Work with Emmett